Chapter 1: Population and Crises

This year again, the Global Humanitarian Assistance Report builds a comprehensive picture of humanitarian trends in the past year. The first chapter of the report focuses specifically the intersectionality of vulnerabilities. The main message of the chapter is that humanitarian needs have increased significantly as a result of more protracted crisis and the combination of escalating/emerging conflicts, socioeconomic fragility, and vulnerability to climate. To address these situations, they recommend a joined-up approach that addresses both immediate humanitarian need and the varieties of risks and shocks (conflict, climate,…) through development projects.

In 2021, the focus has been rather on pandemic recovery than on humanitarian assistance. Yet, humanitarian assistance is ever-more needed with the number of countries with high levels of humanitarian needs increasing from 40 to 49 between 2020 and 2021, 36 countries experiencing protracted crisis and the overall number of people in need of assistance reaching 306 million, 90.4 million more than before the Covid-19 pandemic.

The report highlights the intersecting dimensions of risks, especially between climate change and conflicts. 2/5 people in need of assistance live in countries facing a combination of high intensity conflict and high levels of vulnerability to the impacts of climate change which exacerbates humanitarian needs as it reduces resilience and increases reliance on assistance thus creating long term vulnerability.

Regarding food insecurity, a driver of humanitarian need, the report shows the 28% increase of people experiencing higher level of food insecurity. This trend is concentrated in a few countries, DRC, Afghanistan, Nigeria and Yemen, highlighting a relationship between high food insecurity and conflicts.

Lastly, the first chapter of the report looks at 2021 trends of forced displacement. Once again, the number of forcibly displaced people grew for the tenth consecutive year (+4.7%) mostly explained by conflict escalations in Ethiopia, Afghanistan, South Sudan and Yemen, shocks related to climate change and the worsening economic hardship in Venezuela. Internally displaced people (IDPs) represent a 11% increase from 2020 and refugees are only 1/3 of the total displaced population. Similarly to previous years, half of DPs are concentrated in 10 countries with Syria, Colombia and DRC hosting the largest numbers.

Lastly, the first chapter of the report looks at 2021 trends of forced displacement. Once again, the number of forcibly displaced people grew for the tenth consecutive year (+4.7%) mostly explained by conflict escalations in Ethiopia, Afghanistan, South Sudan and Yemen, shocks related to climate change and the worsening economic hardship in Venezuela. Internally displaced people (IDPs) represent a 11% increase from 2020 and refugees are only 1/3 of the total displaced population. Similarly to previous years, half of DPs are concentrated in 10 countries with Syria, Colombia and DRC hosting the largest numbers.

Chapter 2 : humanitarian and wider crisis financing

This chapter highlights the marginal increase of humanitarian funding by 2,5% as needs continue to rise.

In 2021, assistance from governments and European Union institutions accounted for 79% of total international humanitarian assistance. This means that only a handful of countries are sustaining a stable donor base as they provide significant volumes of assistance. However, as needs increase and situations vary, donors are faced with difficult choices which can result in de-prioritisation of humanitarian spending. For instance, in 2022, with the war in Ukraine, humanitarian funding has already been diverted to support response in the country.

In terms of needs, it is important to note that it reduced slightly compared to 2020 as less Covid assistance in needed. However, the overall pattern remains; there is a sever underfunding of humanitarian needs and a lot of unmet requirements.

In 2021, there were 48 UN-coordinated appeals, slightly less than than the previous year but 1/3 over the number of total appeal requirements in 2019. The Syrian Refugee Regional Response plan, the Syria Humanitarian Response and the Yemen Humanitarian Response accounted together for 1/3 of total appeal requirements. Moreover, half of appeals received less than half their required funding, 23% of appeals received more than 75% of their requirements. Whilst 71% of country-allocable international humanitarian assistance was provided within UN-coordinated appeals, some fundings are made outside of this framework through Red Cross organisations, NGOs and private sector companies. The largest volume of funding to a country with no UN-appeal was India.

The chapter also analyses humanitarian funding per sector. There are four main observations. First, food security is by far the most funded sector, with almost four times as much funding as any other sector in 2021 and targeted to the largest number of people. This trend has been consistent every year for the past decade. Despite large amounts of funding, requirements for food security keep increasing in 2021 driven by Syria and Ethiopia and in 2022 by the war in Ukraine. Second, “early recovery” (sector seeking to support sustainable recovery from crises and lay the foundations for long-term development) received the least amount of funding. Third, health requirements increased by 62% yet, the nutrition cluster has seen an improvement in the number of requirements met. Finally, the education sector is experiencing a dramatic underfunding over the past four years.

In the final sections of the chapter, there is a particular focus on gender-relevant funding and climate finance flows. In both cases, there are major positive developments with increasing funding and awareness on those issues, however, funding in those sectors still represent a very small proportion of total international humanitarian assistance.

Assistance targeting gender-based violence specifically has increased and accounted for 38% of total gender specific funding, yet only 29% of requirements in the area were met. In terms of gender related needs, the COVID-19 pandemic has increased the requirements, however reporting and data collection remains challenging. Overall, there tends to be no certain ways to identify the volumes of funding required for humanitarian programming relating to gender equality. In 2021, total gender-relevant funding represented only 3.4% of total international humanitarian assistance.

In 2021, half of the people in need of humanitarian assistance, lived in areas facing high levels of vulnerability to the impacts of climate change. In 2020, UN humanitarian appeal requirements linked to extreme weather were eight times higher than 20 years ago. Despite pressing needs, humanitarian assistance linked to climate emergencies is seriously underfunded. As such, the report calls for a better understanding of the mechanisms and objectives of climate finance (uses a range of financing structures and instruments, including a mix of local, national and international resources) to alleviate the severity of climate change through emission-reduction activities and promote the transition to less carbon-intensive economies. The main structure and instruments used are under the UN Framework Convention on Climate Change (UNFCCC). Climate finance differs from other humanitarian assistance as it is ore targeted at disaster prevention than disaster response. The aims of climate finance (averting, minimising, and addressing) are critical to building resilience by managing risks and adapting to change. The report suggests that if climate finance is provided as grant ODA, it can support efforts in countries at risks of protracted crises by supporting key sectors. Overall, there is insufficient funding addressing sudden and slow-onset humanitarian disasters that result from climate change.

Chapter 3 : Donors and recipients of humanitarian and wider crisis financing

This chapter focuses on the donor’s perspectives in a context where the need to widen the donor base for humanitarian assistance and better target finance to countries experiencing crisis has been long established.

The trend in public humanitarian assistance has been a large concentration of funding with the 3 largest donors (US, Germany and UK) accounting for 59% of all public humanitarian assistance. It is important to note changes in individual funding patterns with the UK reducing its funding by 39% from 2020. This significant decrease in funding has been counterbalanced by an increase in excess from US and Germany as well as by the doubling of Japan’s assistance.

Looking at funding for in-country refugee hosting and gender-specific projects, there is a decline in spending for the former which is likely to be reversed in 2022 with refugees fleeing from Ukraine. For gender-specific funding, the 10 largest donors accounted for 88% of total funding on this matter. However, although it is concentrated, the total funding for gender-relevant humanitarian activities has increased significantly. Yet, this increase is not proportional to the rising needs and still represents a very small volume of the total assistance they each provide. For instance, gender-specific assistance from EU institutions and the US is the largest but only accounts for 2% of their total assistance.

In terms of private funding, the total international humanitarian assistance from private donors increased by 5% and the volume of official development assistance (ODA) from multilateral banks doubled since 2015. Individuals were historically the largest source of private funding. This proportion from individuals dropped in 2019 but was offset by a significant increase in funding from other private donors due to the Covid-19 outbreak. Both funding from national societies at country levels and assistance targeted to NGOs remained consistent. Yet, there was an increase from 12% to 19% in private funding provided to multilateral agencies. Private funding is key for successful humanitarian response as it is more flexible and therefore allows organisations to act on underfunded crises/ projects and/or in more complex areas.

Overall, the donor landscape remains largely similar to previous years: a small number of donors provide 97% of all international humanitarian assistance

Another way to look at donor’s behaviour and strategies in terms of humanitarian assistance is to focus on the percentage of GNI (Gross National Income) used as humanitarian assistance. In 2021, only 4 donors provided more than 0.1% of GNI compared to 6 in 2020. The overall configuration is becoming increasingly inadequate to growing humanitarian needs. The report suggests policy changes such as increasing the proportion of GNI provided to mobilise significant volumes of humanitarian assistance. In 2021, the US, which is the largest donor and has the highest GNI, only provides 0.04 of its GNI to humanitarian response. Moreover, high income countries that are not part of the largest donors, such as France, South Korea or Australia, should also allocate more of their GNI to humanitarian aid.

Chapter 4 : Recipients and delivery of humanitarian funding

Similarly to the findings of previous chapters, chapter 4 of the report shows that there is a concentration of assistance: the 10 largest recipients received 60% of country-allocable international humanitarian assistance. Overall, the report highlights the need for more effective and efficient delivery of assistance.

The list of the 10 largest recipients remained largely unchanged, except for Nigeria, and Afghanistan entering the list and displacing, as a result, Turkey and Iraq. Overall, in 2021, 144 countries received some humanitarian assistance which is 20 fewer than in 2020. Channels of funding also remained relatively similar to the past years.

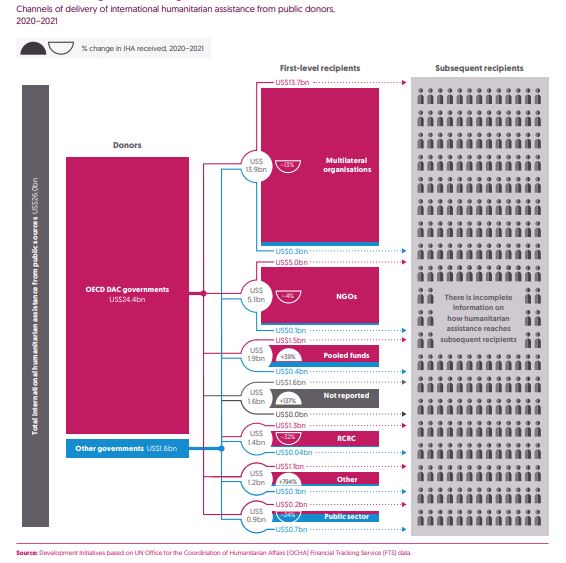

Most assistance from public donors (54%) went through multilateral organisation (despite a slight decrease as a proportion of total assistance). 19% of total contribution went to NGOs, making it the second largest recipient. The main donors providing assistance through NGOs and multilateral organisation is still governments from the OECD’s Development Assistance Committee (DAC OECD). Funding outside of this channel increased thanks to the assistance from Saudi Arabia and the United Arab Emirates but still represent only 6.5% of total assistance from public donors. It is important to note that the public sector is mainly financed by non-DAC donors who represent 42% of its funding.

Local and national societies also represent an important recipient of humanitarian assistance. Whilst this has been a priority of the Grand Bargain 2.0 strategy, direct funding to local actors spiked during the Covid-19 response and dropped significantly in 2021 in both volume and as a share of total assistance. Important volatility in volumes of direct funding is mostly driven by fluctuation in funding to national government. For instance, the 2019 drop was caused in part by the 70% decrease in the funding to the government of Yemen. The nature of funding – through an intermediary to reach local and national actors – makes it hard to collect data and successfully assess patterns and trends. There is therefore a clear need for better reporting of financing to help improve analyses of progress of delivery.

So far, the available data suggests that most funding to local and national NGOs is indirect. Although there was a slight increase in volumes of direct funding to local and national NGO, the overall share of funding to NGO distributed to local and national actors has fallen.

Looking at the data of assistance to local and national actors provided by sector, we can observe a peak in 2020, driven by the health cluster, and a drop in 2021 in all sectors. The food security cluster has grown steadily since 2019 however, as a proportion of total funding to the food security cluster, only 3% is distributed to local and national actors.

The report identifies three barriers that prevent funding to reach local communities directly: the type of funding, the funding system which puts local actors as sub-contractors to international organisation and the overall reliance on short-term humanitarian funding cycles which prevents equitable partnerships. Those barriers impede on locally led delivery and does little to facilitate locally led coordination which increases reliance on bigger organisations and vulnerability of local actors. As such, it is necessary not only to remove those barriers to funding but also increase the quality of this funding by promoting more locally led responses.

In 2021, unearmarked funding to UN agencies declined to the smallest proportion in 6 years (13% of total funding), far behind the commitment of the Grand Bargain for 30% of donor funding to be provided unearmarked. This decrease was primarily driven by a reduction in allocation to the World Health Organisation after the increase for Covid response. Only three UN agencies followed the commitment of the Grand Bargain: UN OCHA, UN HCR and UN Relief Work Agency for Palestine Refugees in the Near East.

Multi-year funding is important to increase the quality of the funding. Whilst there have been efforts to increase the volumes of multi-year funding, the amounts are not enough to enable transformative change within the sector. This is due to the lack of common understanding of the benefits of multi-year funding in terms of programs and of the best target for allocation to achieve the greatest impact. There is overall limited data and reporting to have a comprehensive picture of multi-year funding.

Finally, another channel of funding has been through humanitarian cash and voucher assistance which has been increasing in the last six years. In 2021, cash and voucher assistance made up 19% of total international humanitarian assistance, mostly provided by UN agencies which account or 61% of total cash and voucher assistance. The majority (71%) was provided in cash, the preferred delivery modality, and 29% as vouchers. This growth in cash and voucher assistance led to the emergence of multipurpose cash clusters (MPC) in some response plans, which have been use recently in Ukraine for instance.

Summary by Eva Miccolis.

You must be logged in to post a comment.